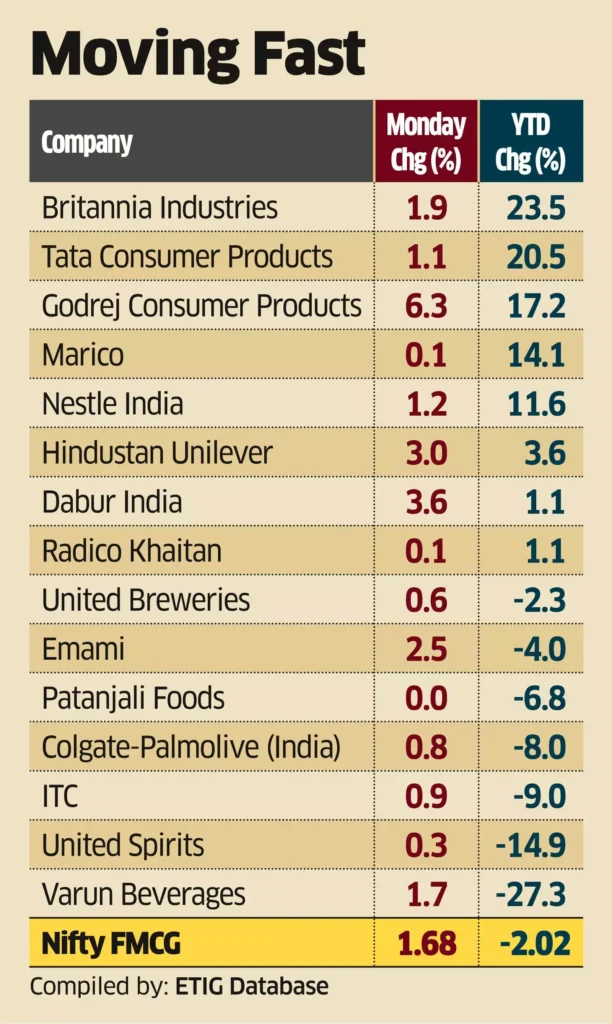

Currently, Hindustan Unilever (HUL) holds a valuation near Rs 5.31 trillion, slightly surpassing ITC, which stands at about Rs 5.13 trillion.

This puts HUL slightly in the lead in the race to reach Rs 10 trillion. Nonetheless, the key question remains:

which company will be able to continuously grow its earnings at a faster and more consistent pace? HUL is akin to a smooth, rhythmic runner in the realm of pure-play FMCG, boasting less drama and more predictability.

In contrast, ITC resembles a versatile athlete, possessing multiple strengths and levers, but with a greater number of moving parts involved.

The route they choose and the landscape they favor differ from one another. Below is an analysis of the potential for these two businesses…

Two distinct machines pursuing the same objective.

Hindustan Unilever Limited (HUL) stands as India’s foremost pure-play FMCG company, marked by its expansive portfolio and formidable brand strength across more than 50 brands in 15 categories.

The company holds leadership positions in over 85% of these categories, with 19 of its brands achieving annual sales exceeding Rs 10 billion. HUL’s distribution network extends to over 9 million outlets nationwide, facilitated by engaging approximately 1.4 million retailers through a digitized route-to-market strategy, which enables the company to capture about one-third of its demand digitally.

This strategic combination of extensive brand presence, wide-reaching distribution, and efficient digital execution positions HUL with a significant competitive advantage. In contrast, ITC operates with a diversified profit engine, showcasing a different business strategy.

The core of the company’s operations lies in its cigarette business, while the FMCG sector represents a sustained avenue for growth through consumer franchises.

Additionally, the agriculture and paperboard divisions contribute valuable cash flow and flexibility. To make the FMCG sector more future-oriented, the company is strategically acquiring smaller entities that align with its primary business model and can rapidly scale via existing manufacturing, sourcing, and distribution networks.

With the hotel’s business now demerged and listed separately, the core operations have become more transparent.

The company is thus structured into two distinct models: one focuses on consistent compounded growth, and the other embraces a multi-faceted compounding strategy.

The trajectory towards achieving a valuation of Rs 10 trillion will ultimately depend on market preferences in the upcoming phase, whether they lean towards steady, streamlined operations or diversified cash flow generation.

Who is most likely to reach a valuation of Rs 10 trillion first?

If markets continue to favor steady and straightforward compounding, HUL maintains its lead.

On the other hand, if the focus shifts to appreciating diversified cash generators that show clear scaling, ITC is poised to leap ahead.

Achieving Rs 10 trillion, however, will depend on a lasting rural recovery, favorable input costs, and consistent execution in transforming digital and physical distribution into profitable growth.

Conclusion

The market seldom perpetually benefits the same characteristics.

When the cycle leans towards stability, the focused compounder typically prevails. Conversely, if the cycle prioritizes cash generation from various avenues, the diversified company may gain an advantage quickly than anticipated.

The key is distinguishing the narrative from the actual figures. Wishing you successful investing.

(Disclaimer: The information provided here is for informational purposes only and does not constitute investment advice. The stockshope.org does not offer investment recommendations. The stock market involves risk—please consult a certified investment advisor before making any investment decisions.)